Fill Out Your Wisconsin Pc 200 Template

Fill Out Your Wisconsin Pc 200 Template

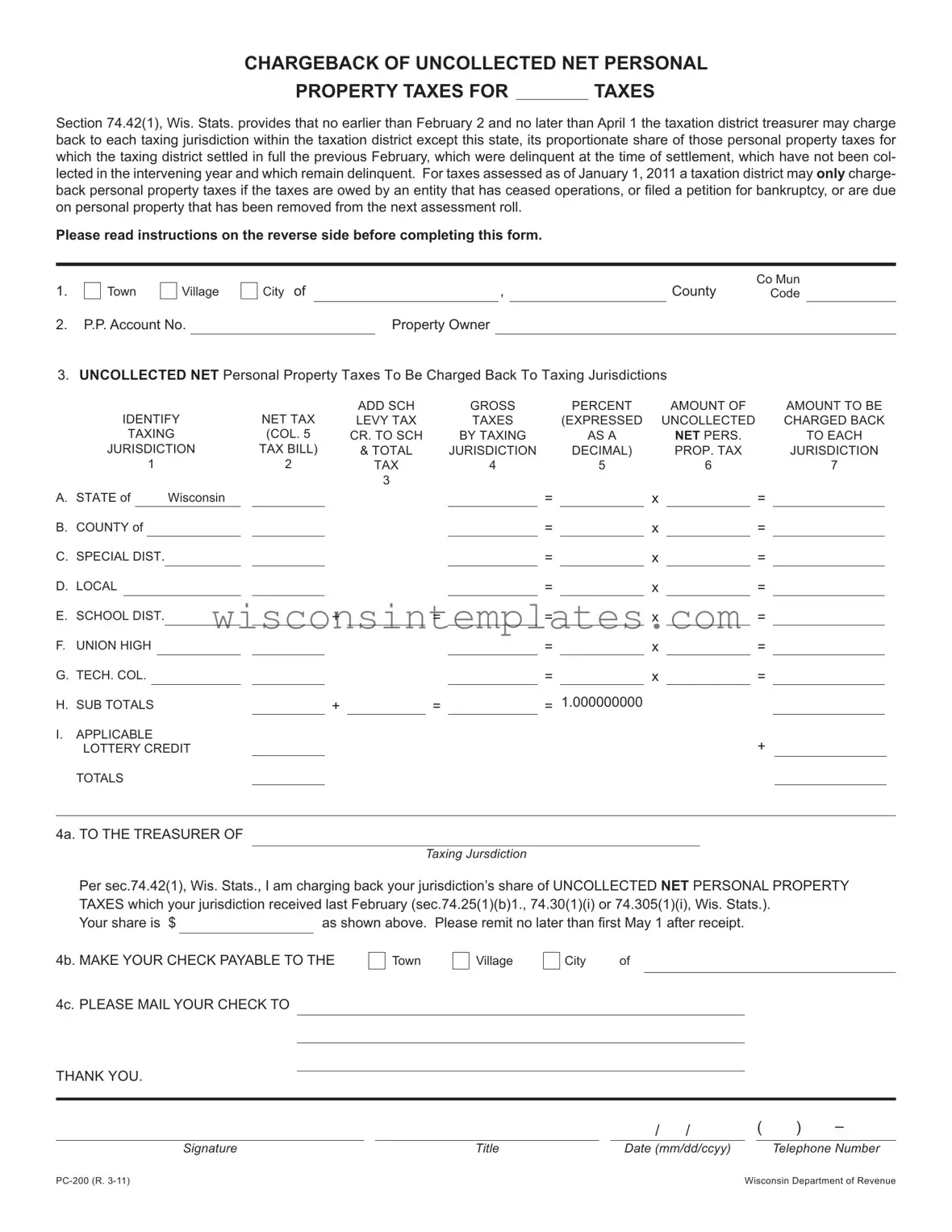

The Wisconsin PC 200 form plays a crucial role in the management of uncollected personal property taxes within taxation districts. This form allows taxation district treasurers to charge back a proportionate share of these taxes to each taxing jurisdiction, excluding the state, during a specified time frame between February 2 and April 1. It addresses situations where personal property taxes, settled in full the previous February, remain uncollected due to delinquency. Notably, for taxes assessed as of January 1, 2011, the form can only be utilized when the owed taxes are linked to entities that have ceased operations, filed for bankruptcy, or involve personal property removed from the next assessment roll. Completing the PC 200 requires careful attention to detail, including accurate calculations of the uncollected net personal property taxes owed by each jurisdiction. The form also includes specific instructions for filling it out correctly, emphasizing the need for clarity in reporting and accountability among taxing jurisdictions. Timely submission is essential, as jurisdictions must remit payment by May 1 following receipt of the chargeback notice. Understanding the intricacies of this form can significantly impact local government finance and tax collection efforts.

Completing the Wisconsin PC-200 form requires careful attention to detail. This form is used for charging back uncollected net personal property taxes to the appropriate taxing jurisdictions. Follow the steps below to ensure accurate completion.

After completing the form, it’s essential to ensure that all calculations are accurate and that the form is submitted on time. If any questions arise during the process, contacting the Department of Revenue for assistance can provide clarity and guidance.

When filling out the Wisconsin PC 200 form, it is essential to understand the following key points:

For further assistance, contact the Department of Revenue's Local Government Services Section.

What Age Do You Stop Paying Property Taxes in Wisconsin - A checkbox is provided for claimants to indicate if they or their spouse were disabled during the year 2021.

A Georgia Hold Harmless Agreement is a legal document designed to protect one party from liability for potential damages or injuries that may occur during a specified activity or event. This form establishes a mutual understanding between the parties involved, ensuring that one party will not hold the other responsible for certain risks. By utilizing this agreement, individuals and organizations can promote safer interactions while clearly outlining their responsibilities. For more information, you can visit formsgeorgia.com.

Wisconsin Mv2449 - Keep the fee payment method in mind when submitting the application.

Iris Wisconsin - Essential contact details for support coordinators are captured to facilitate communication throughout the service period.

When dealing with the Wisconsin PC-200 form, there are several other forms and documents that may be necessary to complete the process effectively. Understanding these documents can help ensure that all requirements are met and that the chargeback of uncollected personal property taxes is handled properly.

Gathering these documents alongside the Wisconsin PC-200 form is crucial for a smooth chargeback process. Each document plays a significant role in ensuring compliance with state regulations and maintaining transparency between taxing jurisdictions and property owners.