Fill Out Your Wisconsin W706 Template

Fill Out Your Wisconsin W706 Template

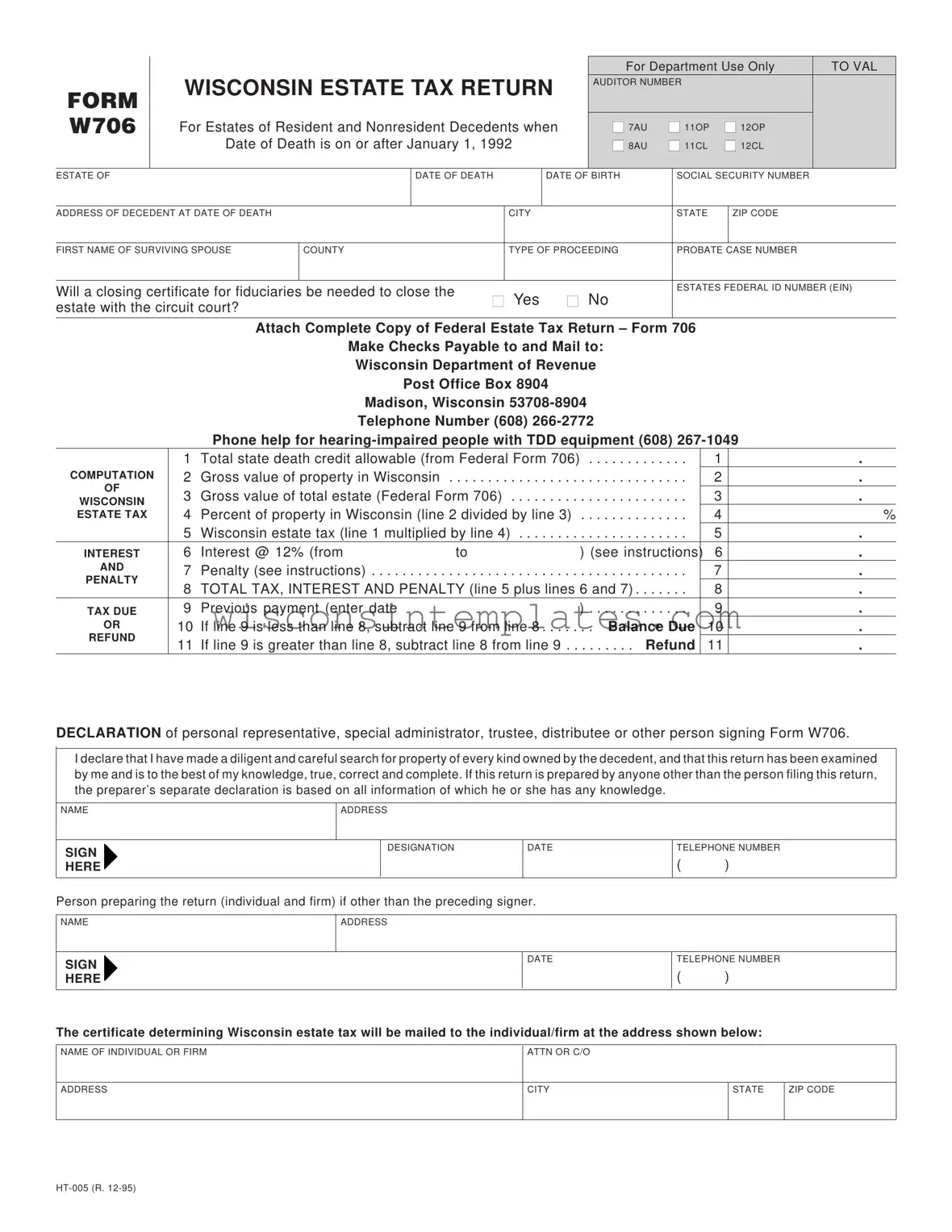

The Wisconsin W706 form plays a critical role in the estate tax process for both resident and nonresident decedents. This form is essential for reporting the estate's value and calculating the applicable taxes owed to the state. If the date of death occurs on or after January 1, 1992, the W706 must be completed and submitted. Information required on the form includes the decedent's date of birth, social security number, and address at the time of death, as well as details about the surviving spouse and the probate case number. The form also prompts the filer to determine if a closing certificate for fiduciaries is necessary to finalize the estate with the circuit court. To accurately assess the estate tax, the gross value of property located in Wisconsin must be calculated, alongside the total estate value reported on the federal estate tax return, Form 706. The W706 then guides the taxpayer through the computation of the Wisconsin estate tax, including any interest or penalties that may apply. Finally, the form requires a declaration from the personal representative or other authorized individual, affirming that a thorough search for the decedent's property has been conducted and that the information provided is accurate and complete. Understanding the nuances of this form is crucial for ensuring compliance and facilitating a smoother estate settlement process.

Filling out the Wisconsin W706 form is an important step in the estate tax process. After completing the form, it will need to be submitted to the Wisconsin Department of Revenue along with any necessary documentation. Here’s how to fill it out step by step.

When dealing with the Wisconsin W706 form, understanding the key aspects can simplify the process significantly. Here are some important takeaways:

By keeping these points in mind, you can navigate the W706 form more effectively, ensuring compliance with Wisconsin estate tax regulations.

Wisconsin Mv2449 - Permits are valid for a period of 72 hours from the date of certification.

Wisconsin Department of Revenue Forms - Engage board members in the financial reporting process for comprehensive oversight.

When dealing with the Wisconsin W706 form, it's essential to understand that several other documents often accompany it. These forms help provide a complete picture of the estate's financial situation and ensure compliance with state regulations. Below is a list of some commonly used forms that you may encounter in this process.

Understanding these forms and their purposes can simplify the process of managing an estate. Each document plays a vital role in ensuring that all legal requirements are met and that the estate is settled according to the decedent's wishes. Having everything organized can make a challenging time a bit more manageable.